Strategic Imperatives

Lynas Rare Earths Limited (LYC) is shifting its identity. The company transforms from a cyclical miner into a core strategic infrastructure asset.1 It remains the world’s only significant producer of separated rare earths outside of Chinese control.2 This unique market position dictates a strategic premium in its valuation.

Western governments mandate supply chain resilience for advanced defense and clean energy technologies.3 This necessity elevates LYC’s role far above conventional commodity fundamentals. The “Towards 2030” strategy confirms aggressive capacity expansion plans.4 Key growth targets include expanding NdPr production to 12ktpa and securing Heavy Rare Earth (HREE) separation capabilities.5

Direct financial backing and binding contracts from the U.S. Department of Defense (DoD) and Japan confirm LYC’s strategic indispensability.7 Traditional valuation models fail when supply security becomes a national security issue.9 Government financing and mandated offtake agreements stabilize the revenue stream, creating defensible, non-market-driven value for the company.10

I. Geopolitical Anchoring: The Western Alliance Mandate

A. Friend-Shoring Fuels Allied Capital Investment

U.S.-Australia diplomatic discussions now focus on urgent strategic negotiations.11 These talks move beyond broad defense themes to address immediate economic dependencies. Washington actively seeks a critical minerals deal to diminish China’s market control.12 This resource diplomacy represents a pivotal moment in global supply chain vulnerabilities.

The U.S. DoD provided a $120 million contract to Lynas to establish domestic HREE separation capacity 7 This contract is critical infrastructure validation. It confirms LYC’s vital role in securing materials essential for U.S. defense applications.3

Japan also demonstrated its strategic commitment. The Japan Organization for Metals and Energy Security (Jogmec) provided A$200 million via JARE in financing.8 This capital ensures priority NdPr supply for Japan until 2038.13 This long-term commitment directly supports the balance sheet and major growth projects.8

Australia committed A$1.2 billion to a Critical Minerals Reserve.14 This structure relies on forward contractual supply frameworks, not physical storage.15 LYC stands to benefit from this secure funding channel and shared ownership structure with allies.16 Allied governments are effectively mitigating LYC’s market risk through state-backed financing.8 The strategic premium attached to non-Chinese supply is monetized through defense contracts and sovereign agreements.10

B. Containing China’s Market Leverage

China’s implementation of export controls on materials like gallium and germanium escalated geopolitical tensions significantly.11 Beijing maintains control over nearly 90% of global rare earth refining capacity.18 This dominance allows China to use strategic materials as diplomatic leverage.11

China previously accounted for 99% of global HREE processing.20 This near-monopoly created the most severe chokepoint for U.S. defense supply chains.3 The intensifying U.S.-China geopolitical rivalry directly spills into the critical minerals realm.9

U.S. government officials are now actively engaging Australian miners on mechanisms for taking “equity-like stakes” in strategic projects.17 This approach represents a fundamental shift. It signals strategic participation over traditional arms-length procurement models.22 This strategy acknowledges that the US-China rivalry forced Australia’s strategic choice.9 Since LYC is integral to Western security, allied governments must bear capital risk to ensure project delivery. This stabilizes LYC’s financial foundation regardless of short-term commodity cycles. Capital injections are targeting infrastructure development, accelerating midstream processing capacity.12 China’s leverage resides in processing capacity.18 Funding LYC’s refineries bypasses market construction timelines, rapidly building the industrial base required for decoupling.

II. Macroeconomic Catalysts and Market Decoupling

A. Price Action and Structural Cost Advantages

NdPr oxide prices surged approximately 40% in recent months, reaching $88/kg (632,000 yuan/tonne) in China.25 This sharply reverses a prolonged period of depressed pricing that plagued the sector in 2024. 26 The rally was unexpected by many market observers.25

The primary catalyst was MP Materials halting raw material exports to China.25 This single event created a significant supply gap, exposing the extreme fragility of the refined market.25 This disruption highlights how small supply changes can trigger outsized price movements.

LYC demonstrated exceptional resilience in 2024. Despite sharp price drops across the rare earth sector, LYC retained a positive margin for refining.26 This operational success contrasts starkly with widespread sector financial losses.26 Furthermore, the DoD established a 10-year price floor (US$110/kg for NdPr).5 This provides a strategic benchmark that guarantees economic viability for key Western projects.5

Extreme price volatility creates instability that only sovereign-backed suppliers can reliably navigate.25 High volatility drives risk-averse defense and automotive industries to prioritize security over spot price. LYC’s integrated supply chain and sustained positive margins validate its ability to sustain production during downturns, securing long-term customer commitments.26

B. Demand Supercycle and HREE Value

Analysts forecast robust demand growth for NdPr, projecting a 10% annual increase through 2030.4. The electric vehicle (EV) and wind power sectors are the dominant demand drivers.4 The NdPr supply deficit is forecasted to persist through 2027.5 These supply gaps underscore the urgency and value of LYC’s expansion plans.5

The Heavy Rare Earth market segment also shows strong growth potential. The Dysprosium market, valued at US$540 million in 2024, is projected to grow at a 6.6% CAGR.29 Price forecasts suggest Dy oxide could climb 450%, reaching $1,400/kg under strategic premium scenarios.28

The successful A$750 million equity placement in August 2025 demonstrates strong market confidence.2 This capital raise mitigates project execution risk. Investors view the macro and geopolitical alignment as overriding the price volatility seen in 2024. 26 This funding supports the large capital investment plan required for the “Towards 2030” growth strategy.4

III. Technology and Science: The HREE Breakthrough

A. Operational Integration and NdPr Scale

The geological advantage of the Mt Weld deposit provides exceptionally high rare earth grades.2 This high-grade feedstock reduces operational costs and minimizes the environmental footprint compared to many global peers.30

The Kalgoorlie Rare Earths Processing Facility represents Australia’s first downstream processor.21 This facility performs the crucial initial cracking and leaching process. It produces Mixed Rare Earth Carbonate (MREC) for further separation.24

Lynas actively expands its global processing footprint. Nameplate NdPr capacity has been uplifted to 10.5ktpa through Malaysian upgrades.4 The Mt Weld expansion is sized to support a final target of 12ktpa of finished NdPr product.5

B. Scientific Advancement in HREE Separation

Lynas achieved a monumental technical milestone with the first production of separated HREE oxides (Dysprosium and Terbium) in Malaysia.21 This proprietary HREE separation circuit provides a production capability of up to 1,500 tonnes per year.31

This capability provides the first scalable, non-Chinese source for these defense-critical materials. 20 HREE separation defines LYC’s strategic moat.31 HREEs command the highest premium and are the most sensitive elements for high-performance defense systems.21 China specifically restricted HREE exports due to their criticality.20 Successfully replicating this complex separation science outside China eliminates the West’s key military supply vulnerability.

Lynas provides assured provenance, essential for defense procurement standards.2 This means customers receive fully traceable rare earth products, traceable from the Mt Weld mine to the final separated oxide.2

C. High-Tech Downstream Integration

The October 2025 partnership with U.S.-based Noveon Magnetics creates a full mine-to-magnet supply chain.1 This alliance integrates LYC’s oxides directly into Western permanent magnet manufacturing.21

China dominates magnet manufacturing, creating a secondary downstream bottleneck.18 The Noveon MoU mitigates this chokepoint. It secures Western industrial capacity using verified non-Chinese materials.1 The operational model features geographic diversification.24 If regulatory or operational issues affect one site (e.g., Malaysia 32), the upstream (Mt Weld) and downstream (U.S.) components ensure continuity and redundancy for allied supply.24 Diversifying processing capacity across multiple friendly jurisdictions minimizes single-point-of-failure risk.

IV. Operational Execution and IP Defense

A. Project Headwinds and Mitigation

The U.S. Heavy Rare Earth facility in Seadrift, Texas, faces known permitting uncertainty.33 A wastewater management issue affects the site, requiring an alternative pathway and additional CAPEX.33 The need for the U.S. HREE facility is driven entirely by geopolitical mandates for defense independence.10 This subjects the company to intense political and environmental scrutiny.

Despite these operational risks, the project is moving forward actively with strong U.S. government backing.10 The delay is assessed as operational, not an existential threat, given the project’s national security priority. The Texas delay shows the inherent friction in forcing complex industrial development onto allied soil for strategic resilience.

The recently completed A$750 million placement reinforces the balance sheet.2 This funding supports the large capital investment plan required for the “Towards 2030” growth strategy.4

B. Intellectual Property as a Moat

Lynas actively defends its proprietary processing methods, primarily within the United States Patent Office.35 This robust defense mechanism creates a long-term technical advantage. Granted patents focus on generating rare-earth carbonates and doped cerium oxide particles.36 These patents cover core chemical engineering steps used in its integrated processing chain.24 Protecting this IP against competitors like Shin-Etsu Chemical is crucial for market longevity.35

Patents covering rare earth separation technology 36 represent Lynas’ non-replicable asset. Unlike mineral reserves, proprietary processing know-how creates a sustainable competitive barrier against rivals attempting market entry.35 China restricts technology export for processing.37 LYC’s independent IP ensures that Western producers relying on LYC are shielded from Beijing’s technology leverage, adding significant value to every tonne produced.

V. Cyber Warfare and Strategic Security

A. The Dragonbridge Influence Operation

Lynas was the direct target of the DRAGONBRIDGE influence campaign.32 This campaign is attributed to actors supporting the political interests of the People’s Republic of China (PRC).32 The campaign utilized thousands of inauthentic social media accounts to spread negative narratives.32 Messaging focused on alleged environmental concerns and called for protests against the Texas facility construction.32

The direct and aggressive targeting of a private rare earth company is highly unusual.39 Mandiant confirmed the campaign’s objective was to undermine commercial entities challenging China’s global dominance.38 The campaign also targeted other Western rare earth firms and criticized the U.S. Defense Production Act invocation 38

B. Official Validation of Threat Status

The U.S. Department of Defense (DoD) issued a public statement confirming its awareness of the disinformation campaign targeting Lynas.40 This acknowledgment validates LYC’s strategic significance as the leading non-Chinese challenger.40

Adversarial states exploit legitimate environmental concerns to disrupt Western projects.32 Environmental, Social, and Governance (ESG) compliance is thus transformed into a national security vulnerability if poorly managed. If a project is successfully halted through politically generated disinformation, the strategic objective is met. LYC must maintain demonstrably superior environmental standards to counter this non-kinetic threat.

Direct state-level targeting reinforces the concept that LYC is a national defense proxy.40 This ensures high priority for regulatory assistance and political backing from allied governments to counteract these influence operations.41 The U.S. commitment to defend LYC’s operational stability creates an additional, government-backed layer of business continuity assurance.

VI. Synthesis and Forward Outlook

A. The Lynas Value Equation: A Multi-Domain Assessment

Lynas Rare Earths presents an investment thesis defined by strategic security, mineral wealth, and technological superiority. Its high-grade Mt Weld mine and demonstrated HREE separation capability provide operational advantages.30 Strategic partnerships, notably the “mine-to-magnet” agreement with Noveon 1 and guaranteed supply to Japan 13, secure long-term revenue streams. The stock reflects a core strategic call on accelerating global supply chain decoupling.

B. Strategic Investment Alignment

The aggregation of state-level capital confirms LYC’s role as a strategic proxy for Western independence.

Table 1: Key Strategic Partnerships and Financial Commitments

| Strategic Partner | Investment Type / Mechanism | Geopolitical Domain | Strategic Outcome/Goal |

| United States DoD | $120M HREE separation contract | Geostrategy | Domestic HREE processing capability in Texas 10 |

| Japan (JARE/Jogmec) | A$200M long-term financing | Economics/Geopolitics | Priority NdPr supply guaranteed until 2038 8 |

| U.S. Government | Potential Equity-Like Stakes | Economics/Geopolitics | Accelerated project funding; supply chain resilience 17 |

| Noveon Magnetics (US) | Strategic Partnership MoU | High-Tech/Technology | Creation of fully Western “mine-to-magnet” supply chain 1 |

| Australia Government | Major Project Status; A$1.2B Reserve | Macroeconomics | Domestic processing support; strategic supply framework 14 |

C. Conclusion: Valuation in a Decoupled World

Lynas Rare Earths dominates the non-Chinese rare earths landscape.2 Its valuation is fundamentally tied to the necessity of securing these critical minerals against escalating geopolitical risks.9 While operational execution challenges persist (e.g., Texas permitting issues 33), robust governmental support mitigates these risks substantially. Direct targeting by state-aligned influence campaigns 40 confirms the company’s critical security status. LYC’s success is intrinsically linked to the West’s collective effort to achieve industrial and military mineral independence, solidifying its status as an indispensable global strategic investment.

References

- Lynas Rare Earths and Noveon Magnetics: The Alliance That Could Redefine Western Magnet Supply

- Lynas Rare Earths: Home

- Developing Rare Earth Processing Hubs: An Analytical Approach – CSIS

- Lynas Rare Earths: Scale Achieved-Now for Sustainable Returns

- Why Lynas, Iluka and rare earth stocks have more than doubled in recent months

- Lynas FY25 Results and Towards 2030 Strategy Presentation – Lynas Rare Earths Limited (ASX:LYC) – Listcorp.

- Critical minerals, clean energy and a US compact

- Australian rare earths miner Lynas receives $133m from JARE – Mining Technology

- Australia’s Critical Minerals Strategy amid US–China Geopolitical Rivalry – RUSI

- DoD Awards Key Contract for Domestic Heavy Rare Earth Separation Capability

- Albanese Trump Meeting Timing Transforms Critical Minerals Strategy – Discovery Alert

- Five things to know about Australia’s critical minerals – Space Daily

- Lynas share price rebounds on $200m Japanese Government investment – Motley Fool

- Australia’s A$1.2 Billion Critical Minerals Strategic Reserve Secures Supply Chains – Discovery Alert

- Australia Moves to Establish Strategic Critical Minerals Reserve as Global Trade Tensions Rise – Small Caps

- Australia’s Path to Critical Minerals Superpower Status in 2025 – Discovery Alert

- Australia Rare Earths Supply to US: Strategic Partnership – Discovery Alert

- Rare Earth Processing 2025 – Global Capacity and Key Players

- China’s New Rare Earth and Magnet Restrictions Threaten U.S. Defense Supply Chains – CSIS

- The Consequences of China’s New Rare Earths Export Restrictions – CSIS

- LYC | China’s Rare Earths Clampdown: Lynas Shares Hit $20B Market Cap

- US offers to purchase stakes in Australian critical mineral companies – Energy News

- US Offers to Buy Stakes in Australian Critical Minerals Companies – Discovery Alert

- Kalgoorlie, Western Australia – Lynas Rare EarthsKalgoorlie Rare Earths Processing Facility

- Neodymium and Praseodymium Prices Surge 40% Since July 2025 – Discovery Alert

- What will happen to rare earth markets in 2025? – Fastmarkets

- Lynas Rare Earths’ 90% Profit Plunge Prompts A$750 Million Capital Raising – Discovery Alert

- Dysprosium Price Now – Historical Prices – 2025 Forecast – Strategic Metals Invest

- Dysprosium – Rare earth elements market outlook – Grand View Research

- Lynas’ Multi-Billion Dollar Rare Earths Expansion Amid Global Tensions – Discovery Alert

- Lynas becomes first producer of heavy rare earths outside China – MINING.COM

- Pro-PRC DRAGONBRIDGE Influence Campaign Targets Rare Earths Mining Companies in Attempt to Thwart Rivalry to PRC Market Dominance | Mandiant | Google Cloud Blog

- Lynas Rare Earths FY2025 Results Announcement – Listcorp

- US Project Updates – Lynas Rare Earths

- Lynas Rare Earths sees highest patent filings and grants during May in Q2 2024 – Mining Technology

- Patents Assigned to Lynas Rare Earths Limited

- U.S. Considers Stake in Australian Miners to Cut China Reliance – Trading Economics

- Chinese hackers use Dragonbridge campaign to target rare earth mining companies

- Fake online accounts targeted rare earths projects – POLITICO Pro

- Chinese influence operation aimed to protect Beijing’s stake in rare earth mining, research finds | CyberScoop

- Reports of Disinformation Campaign Against Rare Earth Processing Facilities

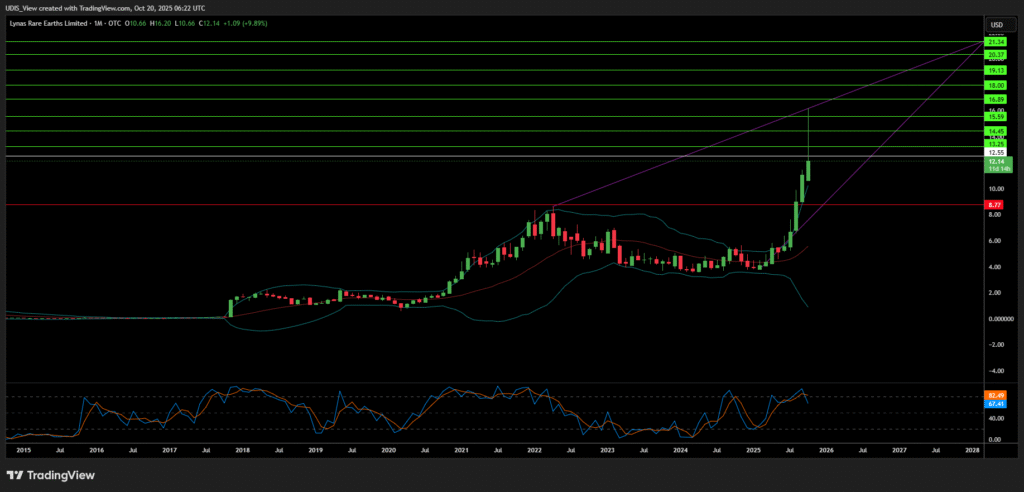

Lynas Rare Earths Limited Long (Long)

Enter At: 12.55

T.P_1: 13.25

T.P_2: 14.45

T.P_3: 15.59

T.P_4: 16.89

T.P_5: 18.00

T.P_6: 19.13

T.P_7: 20.37

T.P_8: 21.34

S.L: 8.77