1. The Nuanced Narrative: From Volatility to Resilience

The financial narrative surrounding JD.com, Inc. often centers on its stock price volatility. Market observers have speculated about a company in decline, facing insurmountable challenges. This analysis posits a more complex reality. While external pressures have indeed impacted market sentiment, the company’s core business demonstrates robust, healthy growth. Its operational strength and strategic pivots tell a story of resilience, not decline. This report reframes the conversation, examining the disconnect between the company’s strong fundamentals and its market valuation.

The company’s recent financial performance offers a clear rebuttal to any claims of decline. JD.com reported significant growth in both revenue and profitability throughout 2024 and into 2025. In the fourth quarter of 2024, net revenues rose by 13.4% year-over-year.1 This growth accelerated in 2025, with a 15.8% increase in net revenues in the first quarter and a 22.4% increase in the second quarter compared to the same periods in 2024.3 Full-year 2024 revenues were RMB 1,158.8 billion, a 6.8% increase from 2023.1

JD.com has also significantly improved its operational efficiency and profitability. The operating margin for the full year 2024 was 3.3%, a notable increase from 2.4% in 2023.1 This positive trend continued in 2025, with the non-GAAP operating margin reaching 3.9% in the first quarter.3 JD Retail, the company’s core business, saw its operating margin improve to 4.5% in the second quarter of 2025.4 The company’s strong financial footing is further evidenced by its proactive share repurchase program, with approximately $3.6 billion in repurchases during 2024 and an additional $1.5 billion in the first half of 2025.2 These actions reflect management’s confidence in the company’s underlying value and long-term prospects.

This table provides a data-driven overview of JD.com’s core financial health. It serves as the foundation for the analysis, presenting empirical evidence that the company is demonstrating substantial operational strength.

| JD.com Key Financials (RMB Billions) | Q4 2024 | FY 2024 | Q1 2025 | Q2 2025 |

| Net Revenues | 347.0 | 1,158.8 | 301.1 | 356.7 |

| YoY Growth | 13.4% | 6.8% | 15.8% | 22.4% |

| Operating Income | 8.5 | 38.7 | 10.5 | 8.5 |

| Operating Margin | 2.4% | 3.3% | 3.5% | 2.4% |

| JD Retail Operating Margin | 3.3% | 4.0% | 4.9% | 4.5% |

2. Domestic Headwinds and Economic Realities

The perceived challenges for JD.com are inseparable from China’s broader economic environment and its highly competitive e-commerce market. The macroeconomic landscape presents a complex backdrop for all businesses in the region. China’s GDP grew by 5.0% in 2024, achieving its official target.5 This growth, however, occurred amidst a persistent deflationary cycle. The Consumer Price Index (CPI) rose just 0.2% for the year, far below the 3% target, reflecting subdued domestic demand.5 The Producer Price Index (PPI) has also dropped for 27 consecutive months, highlighting ongoing industrial price pressures.5 This deflationary feedback loop creates a challenging environment for consumption and consumer spending.6

The domestic market is also subject to intense competitive pressures. The Chinese e-commerce landscape, once a duopoly between Alibaba and JD.com, now includes a formidable third player: Pinduoduo.7 Pinduoduo’s business model is a disruptive force, relying on a consumer-to-manufacturer (C2M) approach that cuts out intermediaries and offers ultra-low prices.9 This strategy drove Pinduoduo’s revenue to a staggering 184.4% compound annual growth rate (CAGR) from 2016 to 2021.9 In response to this new competitive reality, the major players have shifted their focus. The Chinese government’s 2025 Anti-Unfair Competition Law, which prohibits “below-cost pricing,” also forces a pivot towards more sustainable models.10

JD.com’s rising operating margins are not an accident but a calculated strategic response. Rather than engaging in a destructive price war with Pinduoduo, JD.com is leveraging its core competencies: a premium brand reputation, a direct sales model, and a robust logistics network.9 This strategic choice prioritizes long-term profitability and operational efficiency over gaining market share at all costs. The company is actively focusing on its bottom line, a move that enhances its resilience and signals a disciplined approach to growth in a competitive and evolving market.

This table provides a snapshot of the competitive landscape, illustrating how the market has evolved beyond a simple duopoly.

| Key Players in China’s E-commerce Market |

| Alibaba: 47.1% (May 2021) 7 |

| JD.com: 16.9% (May 2021) 7 |

| Pinduoduo: 13.2% (May 2021) 7 |

3. The Technological Bedrock: JD.com’s Differentiator

JD.com’s heavy investment in technology and its proprietary logistics network are its most significant competitive advantages. Unlike its competitors, the company has focused on building its own supply chain infrastructure from the ground up.12 This network includes six highly synergized logistics networks: warehousing, line-haul transportation, last-mile delivery, bulky items, cold chain, and cross-border logistics.13 As of late 2024, JD Logistics managed over 3,600 warehouses with a total area exceeding 32 million square meters.13 The company’s in-house logistics allow it to offer premium services like its “211 program,” which provides same-day or next-day delivery for a significant portion of its orders.14

JD.com consistently invests in cutting-edge technologies to enhance this infrastructure. The company has invested a total of RMB 75 billion in research and development (R&D) since 2017.15 This R&D investment has far outpaced its revenue growth in recent years.15 This significant capital expenditure has led to tangible improvements in operational efficiency. For example, its intelligent warehouse technology, which uses sophisticated dispatching algorithms for robots, has reduced the fulfillment expense ratio to a world-leading 6.5%.14 This efficiency has resulted in estimated annual savings of hundreds of millions of dollars.14 The company has also rolled out its “Zhilang” intelligent warehousing system for nationwide application.4

The company’s focus on intellectual property reflects this technological emphasis. JD.com holds a total of 128 global patents, with a primary focus on smart logistics, artificial intelligence, and robotics.16 Its patents include inventions like an “article conveying system” to improve delivery efficiency and a “smart contract” apparatus.17 This patent portfolio demonstrates the company’s commitment to protecting its innovative solutions and establishing a unique market position. The company also uses its “Heaven’s Mirror” system, an AI-driven anti-counterfeiting tool, to identify high-risk products and maintain its reputation for selling genuine goods.11 This focus on authenticity and reliability is a critical differentiator in a market often plagued by counterfeit issues.

4. Geopolitics, Tariffs, and Regulatory Crackdowns

JD.com’s stock volatility is a direct result of geopolitical and regulatory pressures that transcend its operational performance. The US-China trade relationship remains strained, with tariffs and export controls reshaping the global supply chain. In April 2025, the US enacted new tariffs, including a 34% tariff on a wide range of Chinese imports.20 The cessation of the

de minimis exemption, which allowed duty-free imports under $800, further compounded costs for cross-border e-commerce businesses.21 These trade barriers result in higher wholesale costs, reduced profit margins, and a push for businesses to seek alternative suppliers outside of China.20

Concurrently, Beijing has pursued a comprehensive, multi-year regulatory campaign targeting its domestic technology sector. This “crackdown,” which began in 2021, has addressed issues from antitrust and data security to gaming and social media.22 The government’s actions, such as the $2.8 billion fine on Alibaba for monopolistic behavior, are not random acts of hostility.8 Instead, these policies represent a calculated strategy to reassert state control and ensure the tech sector aligns with national objectives.23 The government aims to foster a “disciplined expansion” and reduce reliance on foreign technology.

A clear connection exists between US export controls and Beijing’s push for technological self-sufficiency. For instance, US Commerce Secretary Howard Lutnick’s comments in 2024, downplaying the sale of less-powerful chips to China, reportedly triggered a swift regulatory response.24 Chinese officials viewed the remarks as an insult, reinforcing their long-term goal of fostering indigenous chip development and reducing reliance on American technology.24 This dynamic highlights a critical geostrategic theme: US pressure on technology access is a significant driver of China’s domestic policies, which in turn affect the operating environment for companies like JD.com. This is a crucial element that distinguishes a basic economic analysis from a deeper, more rigorous examination of the market.

5. The Taiwan Contingency: A Geostrategic Analysis

The user’s hypothetical scenario – a US embargo lifted on China due to a Taiwan invasion – is a geopolitical paradox. An invasion would trigger a swift, severe, and coordinated sanctions regime, not a de-escalation or a lifting of trade restrictions.25 The history of US sanctions on China shows that such measures are a direct response to national security concerns and human rights issues, not a reward for military aggression.27 A trade embargo was lifted in 1972 to open diplomatic relations, not to condone conflict.27 An invasion of Taiwan would likely prompt a new, unprecedented embargo of military and economic scope.

The financial consequences of such a conflict would be cataclysmic. Bloomberg Economics estimates a Taiwan invasion would cost the global economy around $10 trillion, dwarfing the impact of the war in Ukraine or the 2008 financial crisis.25 The primary driver of this economic devastation would be the loss of access to Taiwan’s semiconductor chips, which are critical to a multitude of global industries, from electronics to automobiles.25 The economic blow would be extensive: a 16.7% hit to China’s GDP, 40% to Taiwan’s, and a 6.7% decline for the US economy.25

A central component of a US-led sanctions package would be the exclusion of Chinese banks from the SWIFT financial messaging system. This move has been described as “the financial nuclear weapon”.28 Removing a country from SWIFT makes its interbank payments significantly more complex and severely limits its ability to conduct international trade.28 A precedent exists in the sanctions against Russia, which saw a handful of banks delisted from the network.28 For China, a full SWIFT ban would be a systemic shock on a much larger scale, given its deep integration into the global economy as a major trading and manufacturing power. It would not only impede trade but also destabilize its currency and could trigger a mass-scale bank run.29

In a conflict scenario, the US government would also likely freeze Chinese assets on its soil, including corporate bank accounts, bonds, and US-listed stocks.30 Chinese authorities would likely try to preemptively sell their holdings of US securities to avoid this action, causing temporary but significant market disruption.31 This would be a coordinated response with allies, designed to isolate and cripple the Chinese economy.31

6. Consequences for US-Listed Chinese Stocks

The geopolitical risks of a Taiwan conflict pose an existential threat to all Chinese stocks traded on US exchanges. These securities would face simultaneous operational and liquidity crises. Sanctions would prevent Chinese companies from accessing US capital markets and processing transactions in US dollars, effectively paralyzing their international business operations.29 The mere threat of such sanctions would create massive market uncertainty and volatility, increasing the cost of debt and equity financing for affected firms.32 The ripple effects would extend beyond Chinese firms, negatively impacting the stock prices of their American suppliers and business customers as well.32

A conflict would also trigger a forced delisting of Chinese American Depository Receipts (ADRs) from US exchanges. This would render the shares illiquid for US investors, leaving them with no viable mechanism for sale or conversion.30 A massive sell-off would likely ensue, causing a market collapse for all US-listed Chinese firms. This is not a typical market correction but a structural risk specific to the ADR model in a geopolitical conflict. The risk is non-linear and would be determined by political events, not corporate performance.

The fundamental disconnect between JD.com’s strong financials and its volatile stock price highlights a critical investment reality. Traditional financial analysis, relying on metrics like price-to-earnings ratios and revenue growth, is insufficient for valuing US-listed Chinese companies. The primary risk is not operational or competitive; it is geopolitical. Investors are pricing in the possibility of a political black swan event. The true determinant of future value for these securities is the stability of US-China relations, not the strength of a company’s balance sheet. This makes investment in such companies a high-stakes bet on geostrategic stability.

7. Conclusion: Navigating a Volatile Future

JD.com is a resilient and operationally strong company. The evidence from its 2024 and 2025 financial reports shows a business that is not in decline but is in a period of strategic, profitable growth. The company’s heavy investment in its proprietary logistics network and intellectual property provides a durable competitive advantage. This focus on operational efficiency and technology has allowed it to navigate a challenging domestic economy and intense competition from rivals like Pinduoduo.

However, the company’s strong domestic position cannot insulate its US-listed shares from extraordinary geopolitical risk. The fate of these securities is intrinsically tied to the stability of US-China relations. A conflict over Taiwan would trigger a catastrophic financial fallout, rendering these stocks illiquid and potentially worthless for US-based investors. Therefore, while JD.com’s fundamental business remains robust, savvy investors must recognize they are exposed to a political risk premium. The future of US-listed Chinese stocks depends on factors far beyond the control of corporate management. This reality must be a central consideration for any investment in this sector.

Referens

- JD.com Announces Fourth Quarter and Full Year 2024 Results

- JD.com Announces Fourth Quarter and Full Year 2024 Results, and Annual Dividend,

- JD.com Reports Strong Financial Results for Q1 2025 with 15.8% Revenue Growth and Increased Profitability | Nasdaq

- JD.com Announces Second Quarter and Interim 2025 Results

- China Economic Quarterly Q4 2024 and Two Sessions 2025

- Our economic outlook for China – Vanguard

- Who Are Alibaba’s Main Competitors? – Investopedia

- China – eCommerce – International Trade Administration

- A Study of the Success of Amazon, Alibaba, JD.com, Pinduoduo and Meituan – CKGSB Knowledge

- PDD’s Q2 2025 Earnings Outlook: Assessing Profitability Pressures Amid Revenue Growth and Strategic Investment Trade-Offs – AInvest

- Online Brand Protection on JD.com – Wiser Market

- JD.com: Building the Smart Logistic System for the Future – Technology and Operations Management – Digital Data Design Institute at Harvard

- Our Business – JD.com, Inc.

- JD.com: Operations Research Algorithms Drive Intelligent Warehouse Robots to Work

- JD.com: e-Commerce from China to the World – WIPO

- JD.com Patents Key Insights & Stats,

- Patents Assigned to Jingdong Technology Information Technology Co., Ltd. – Justia Patents

- US20210323766A1 – Article conveying system and article conveying method – Google Patents

- Intellectual Property Protection on JD.com – International Trademark Association

- The Impact of US-China Tariffs on Ecommerce and Logistics

- The 2025 U.S.-China Trade War: Impacts on E-Commerce and E-Traders – Pinalloy

- China’s Big Tech crackdown: A complete timeline

- China E-commerce Market Size, Share Analysis & Competitive Landscape 2030

- ‘Deeply Insulting’: How US Commerce Secretary Howard Lutnick’s comments on Nvidia H20 chips has angered China, creating problems for the world’s most-valuable company

- If China Invades Taiwan, It Would Cost World Economy $10 Trillion – Insurance Journal

- Costly Conflict: Here’s How China’s Military Options for Taiwan Backfire | United States Institute of Peace

- United States sanctions against China – Wikipedia

- SWIFT ban against Russian banks – Wikipedia

- Russia’s exclusion from SWIFT: an explainer – Parliament of Australia

- Assets freeze | Security Council – the United Nations

- The Economic Effects of a Potential Armed Conflict Over Taiwan

- Re-examining the costs of sanctions and sanctions threats using stock market data

- Will $41 Trillion in Foreign Assets Exit the U.S.? | Trump’s Policies Rattle Investors

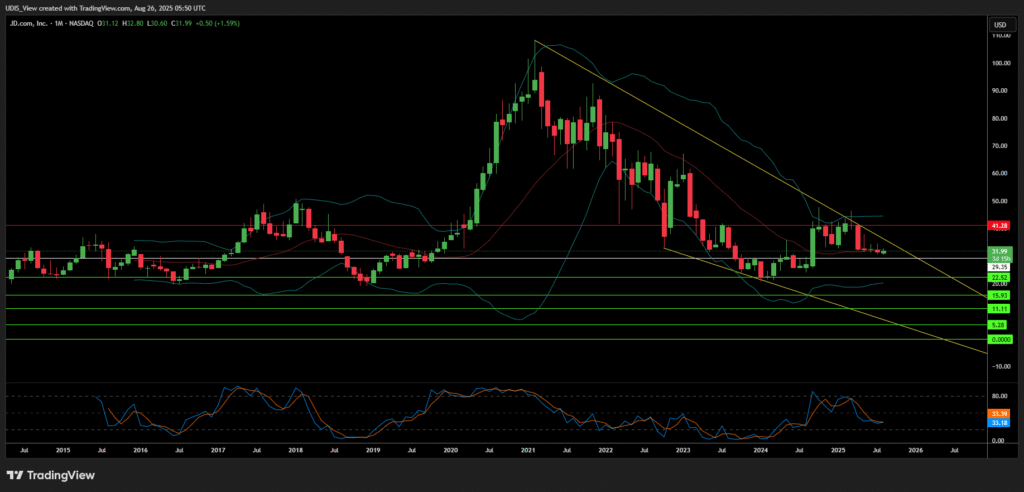

JD.COM Short (Sell)

Enter At: 29.35

T.P_1: 22.52

T.P_2: 15.93

T.P_3: 11.11

T.P_4: 5.28

T.P_5: 0

S.L: 41.28